CRCL Stock Analysis: Can You Buy Circle Now?

Circle Stock Analysis: Is Circle (CRCL) a Good Investment?

Circle (NYSE: CRCL) stands as the first publicly traded company rooted in stablecoin issuance—ushering in a new era where crypto merges with mainstream finance. Founded in 2013 by Jeremy Allaire and based in New York, the firm has evolved into a multi-faceted fintech powerhouse, issuing USDC (USD Coin) and EURC, pioneering a yield-bearing stablecoin (USYC), and building a cross-border payment network (CPN). CRCL’s IPO in early June 2025 ignited investor enthusiasm: it shed light on a business model that blends digital innovation with interest-generating reserve management. This article delivers a full CRCL stock analysis, examines the Circle stock price drivers, and walks readers through how to buy Circle CRCL stock, all while tackling the core question: Is Circle stock a good investment?

Circle: Company Overview & IPO Significance

Circle’s June 5, 2025 IPO drew considerable attention. Priced at $31, shares soared to $83 on debut—an explosive ~168% gain. It ultimately raised over $1 billion, valuing Circle at approximately $7 billion pre-green‑shoe or ~$18 billion post-IPO (moneymorning.com, barrons.com). Backed by heavyweights like BlackRock, Fidelity, and venture capital firms Accel and General Catalyst, Circle’s public debut reflects elevated investor confidence (barrons.com).

What sets Circle apart is its timing. With regulatory headwinds softening—under the SEC’s new leadership and emerging legislation such as the STABLE Act and GENIUS Act—Circle may be one of the first regulatory‑compliant standard-bearers in the stablecoin space. If passed, these regulations could allow Circle to gain a competitive edge by operating with legitimacy and oversight, differentiating from rivals.

Beyond debut hype, the IPO also signals a cultural shift in financial markets—crypto-oriented firms can now tap public capital and gain mainstream validation. As the “first stablecoin stock,” CRCL is viewed as a bellwether for future digital asset innovation in public markets.

Deep Dive: Circle’s Four Core Pillars

Circle’s business rests on four synergistic pillars—each essential in understanding its growth dynamics and risk profile:

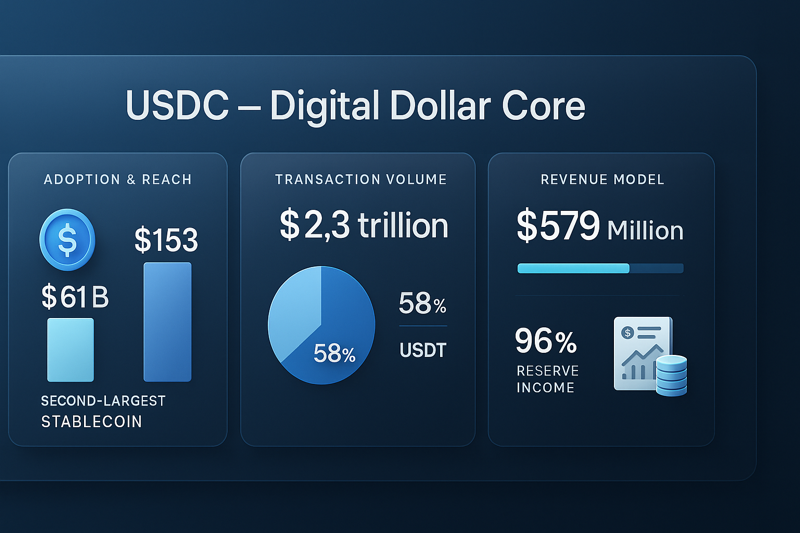

- Adoption & Reach: USDC has roughly $61 billion in circulating supply, making it the world’s second-largest stablecoin after Tether’s USDT (approx. $153 billion).

- Transaction Volume: Its 30-day transaction volume recently topped $2.3 trillion—on par with Visa— and accounted for 58% of total stablecoin trading, compared to 35% for USDT .

- Revenue Model: Circle invests customer deposits in short-term U.S. Treasuries, generating “reserve income”—which comprised nearly 96% of total Q1 2025 revenue ($579 million).

USDC – Digital Dollar Core

EURC – Euro Stablecoin Expansion

- Regulatory Advantage: As the largest issuer of EURC, Circle could dominate the European stablecoin market, particularly if regulations like MiCA continue to be enforced—forcing competitors like Tether to exit major jurisdictions.

USYC – Tokenized Yield Solution

- Mechanics: USYC tokenizes short-term Treasury holdings, offering dollar stability plus interest. It’s now a viable alternative to money-market funds.

- Market Share: USYC holds ~5.5% of tokenized Treasuries, a market recently expanding 400% year-over-year in Q1 2025 .

- Strategic Positioning: This solidifies Circle’s “stability + yield” ecosystem—making asset switching seamless for institutional investors.

CPN – Cross‑Border Payment Network

- Functionality: The CPN enables real-time, low-cost global transfers using Circle stablecoins, bypassing SWIFT’s inefficiency .

- Strategic Growth: Its establishment of compliant cross-border infrastructure strengthens USDC/EURC ecosystem demand.

Summary: Circle’s ecosystem is robust—mapping clear paths from stablecoin issuance to yield products and payment rails. However, USDC’s dominance leaves Circle reliant on macro factors and interest rates. Long-term success depends on scaling USYC and CPN initiatives.

Financial Performance & Metrics

Q1 2025 Highlights

- Revenue: $578.6 million—a 59% YoY increase from ~$365 million in Q1 2024.

- Net Income: $64.8 million, up by roughly 33% from ~$48.6 million in Q1 2024.

- TTM Revenue: Now at $1.89 billion, an extraordinary 983% leap over the prior 12 months.

- Gross & EBITDA Margins: Gross margin stands at ~24%; TTM EBITDA ~$215 million at an 11.4% margin.

- Free Cash Flow: ~$300 million in TTM free cash flow, ~16% margin .

- Balance Sheet: $61 billion in cash/reserves; $53 million in debt—indicating a fortress-like foundation.

Profitability Insights

- Profit margin remains slim at ~1% (TTM), but Q1’s operating margin of ~11% shows improving leverage .

- The diluted EPS is $0.30 on a $133 share price—resulting in a forward P/E that’s not meaningful due to negative per-share profits and volatile earnings.

Stock Performance & Valuation

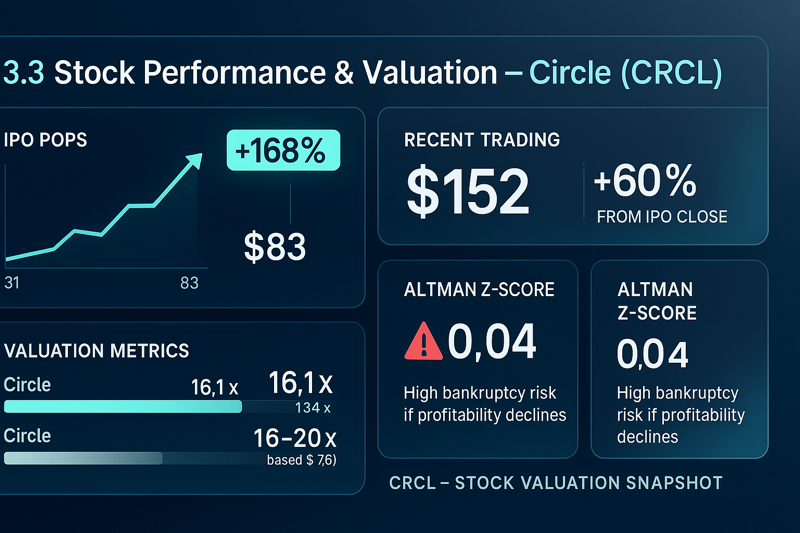

- IPO pops: Shares surged from $31 to $83 on debut—a 168% surge .

- Recent trading: Currently around $152, marking ~60% above IPO close. Volume remains high (~34 million shares/day).

- Price-to-Sales Ratio: At ~16.1× TTM revenue—substantially higher than peers’ ~13.4× average .

- Price-to-Book Ratio: Based on book value/share (~$7.6), CRCL trades at 16–20× book—signalling a premium valuation.

- Altman Z‑Score: 0.04—indicates increased bankruptcy risk if profitability falters.

Analyst Sentiment & Targets

- WallStreetZen & Seeking Alpha: Identify CRCL as overvalued but commend financial strength.

- StockAnalysis: Initiated “Buy” with a $147 fair value—slightly above current levels.

- Zacks: Ranked bottom 44% among its industry in near-term timeliness.

- Barron’s: Notes regulatory openness and strong earnings momentum.

Key Risks for Investors

CRCL’s growth isn’t without vulnerabilities—investors need to weigh key risks:

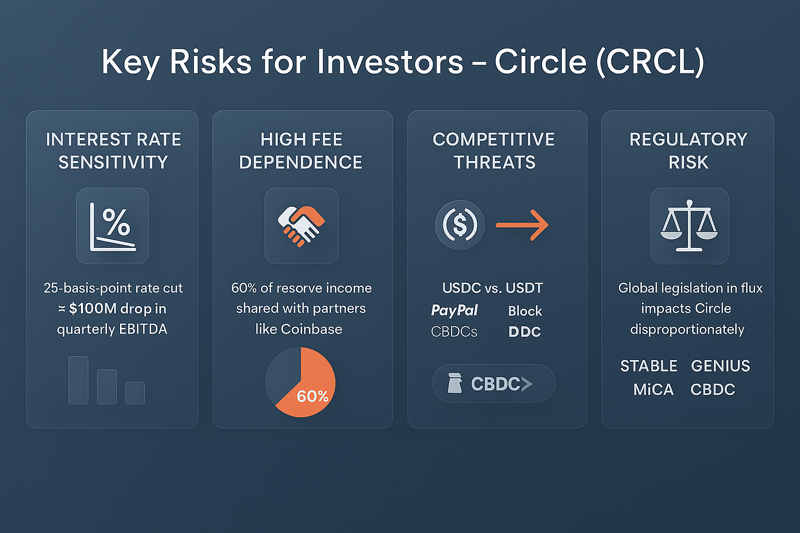

Interest Rate Sensitivity

With nearly all revenue from Treasury yields backing USDC, a 25-basis-point Fed rate cut could strip ~$100 million from quarterly EBITDA—unless offset by deposit growth.

High Fee Dependence

Approximately 60% of reserve income is shared with partners like Coinbase, pressuring profitability. Only increased in-house adoption (CPN, USYC) could alleviate this burden.

Competitive Threats

While USDC ranks second globally, USDT still dominates supply. Additionally, competitors ranging from PayPal, Block, banks, CBDCs, and emerging fintechs can encroach on Circle’s market share .

Regulatory Risk

Regulations like STABLE, GENIUS, MiCA, CBDC frameworks, and global crypto legislation pose uncertainty. While regulatory clarity is growing, any reversal could hurt Circle disproportionately.

Valuation Risk

High multiples mean expectations are lofty. Unless Circle diversifies revenue beyond USDC, disappointments could prompt sharp sell-offs. The Altman Z‑Score and expensive metrics stress the risk.

How to Buy Circle CRCL Stock

If you’re searching “How to buy Circle CRCL stock”, follow this simple guide:

- Pick a Broker: Available through NYSE-capable platforms like Fidelity, E*TRADE, Schwab, Vanguard, Robinhood, and international brokers with U.S. access.

- Fund Your Account: Deposit USD, comply with KYC/AML. International investors may convert currency.

- Search Ticker “CRCL”: Monitor the Circle stock price, identify current bid/ask and price action.

- Place Order: Use Market orders for speed or Limit orders to set your price.

- Follow-Up: After execution, track earnings releases (notably Q2 2025 later in summer), regulatory developments, and usage milestones of USDC/USYC/CPN.

Is Circle Stock a Good Investment?

Upside Potential

- Dominant in Stablecoins: USDC has achieved mainstream adoption and Circle is the leading issuer of compliant digital dollars. Growth in digital finance and cross-border flows benefit it.

- High Margin Model: Investing reserves in Treasury instruments provides a capital-light, high-margin engine .

- Regulatory Tailwinds: Legislation in both U.S. and EU may favor compliant issuers like Circle, helping entrench its leadership .

Warning Signs

- Macro Risk: A recession or policy pivot could crush reserve yields or stablecoin adoption—hitting top-line growth.

- Partner Reliance: Revenue sharing with platforms like Coinbase highlights dependency; margins hinge on renegotiation or direct adoption.

- Competitor & Regulatory Threats: While Circle leads, Tether, banks, and tech giants are formidable challengers. Weighted regulations could change the competitive landscape.

Ideal Investor Profile

- Short-Term Traders: Could benefit from market momentum, ETF inflows, and episodic hype.

- Medium-Term Investors: Watch for performance in USYC/CPN adoption and revenue diversification.

- Long-Term Investors: Should wait for margin improvement, regulatory clarity, and resilience in macro environment before committing heavily.

Verdict

Is Circle stock a good investment?

- ✅ Yes, for traders bullish on digital currency adoption and interest rate stability.

- 🕰️ Maybe, for medium to long-term investors still skeptical of valuation and macro trends. Solid if successful in diversifying income.

Conclusion & Strategic Takeaways

Circle’s IPO marks a new chapter in the convergence of blockchain and traditional finance. It has established strong early momentum: robust revenue and profit growth, a commanding position in stablecoins, and favorable regulatory catalysts. As investors weigh Circle stock price and valuation measures, the CRCL stock analysis supports optimism—especially for interest rate stability and regulatory progress.

However, macroeconomic sensitivity, margin pressure, partner reliance, and expensive valuation make Circle a nuanced investment. Thus:

- Short-term strategy: Leverage momentum and ETF-related flows, but set risk limits.

- Medium-term approach: Wait for Q2 and Q3 earnings to show USYC/CPN traction.

- Long-term discipline: Monitor for margin improvement, regulatory clarity, and diversification of income sources.

Key Investment Highlights at a Glance

| Category | Insight |

|---|---|

| Ticker | CRCL |

| Business Model | USDC, EURC, USYC, CPN |

| Q1 2025 Revenue | $579M (+59% YoY); TTM: $1.89B |

| Profitability | Net Income: $64.8M; EPS diluted: $0.30 |

| Valuation | P/S ~16.1×; P/B ~16–20×; Altman Z‑Score: 0.04 |

| Opportunities | Stablecoin adoption, regulatory tailwinds, yield products, efficient payment rails |

| Risks | Rate cuts, partner fees, competition, valuation premium |

| Investor Considerations | Strong short-term trade; medium-term wait; long-term monitor diversification |

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any financial decisions. We are not responsible for any investment losses incurred based on the information provided in this article.

Pingback: Introduction to Stablecoins: Can you make money with Stablecoin?