NVIDIA Q1 FY2027 Result Analysis: Why Incredible AI Earnings Are No Longer Enough to Shock Wall Street

NVIDIA AI Demand Is Exploding – So Why Isn’t the Stock

NVIDIA Q1 FY2027 earning once again delivered an extraordinary results, reinforcing its dominance at the center of the global AI infrastructure boom. Revenue surged, margins expanded, and hyperscaler demand for AI compute remained exceptionally strong. Blackwell adoption accelerated rapidly across major cloud providers, while management continued emphasizing that AI infrastructure spending is still in the early stages of a multi-year expansion cycle.

Under normal market conditions, results like these would likely have triggered another explosive rally in the stock. Yet the market reaction this time felt noticeably different. Despite another massive earnings beat, investors appeared far less emotional than they were during previous NVIDIA quarters throughout 2023 and 2024.

That shift reveals something important about where the AI investment cycle stands today.

The debate is no longer whether NVIDIA can continue growing. Most institutional investors already assume the company will remain one of the biggest beneficiaries of the global AI buildout. Instead, the real question has become how much future dominance has already been priced into the stock.

This is the psychological transition now happening across AI investing. Markets are moving away from narrative-driven enthusiasm and toward valuation-driven scrutiny. That change may ultimately define the next phase of NVIDIA’s stock performance far more than quarterly earnings beats alone.

NVIDIA’s Financial Results Remain Exceptionally Strong

NVIDIA reported approximately $81.6 billion in quarterly revenue, representing year-over-year growth of more than 85%, while net income surged over 210%. Gross margins expanded to nearly 75%, highlighting the extraordinary profitability of the company’s AI infrastructure business model. Operating cash flow remained enormous, supporting aggressive shareholder returns through dividends and a massive new buyback authorization.

The company’s data center business continued to dominate overall growth, generating approximately $75.2 billion in revenue as hyperscalers raced to expand AI compute capacity. Demand for Blackwell systems remained extremely strong, with virtually every major cloud provider rapidly deploying the platform.

From a business execution standpoint, NVIDIA continues operating at a level few technology companies in history have achieved. The company is not simply selling chips anymore. It is increasingly selling complete AI infrastructure ecosystems that combine GPUs, networking, software, system architecture, and integrated AI deployment solutions.

This system-level approach is becoming one of NVIDIA’s most important competitive advantages as AI infrastructure grows more complex.

Why Explosive NVIDIA Earnings No Longer Create the Same Excitement

One of the most important developments happening in the market today is expectations saturation.

During the earlier stages of the AI boom, investors were still uncertain about several major questions. Would generative AI demand remain durable? Would cloud providers continue increasing CapEx spending? Could enterprises truly monetize AI at scale? Would NVIDIA maintain its leadership position against growing competition?

At that stage, every earnings report reduced uncertainty and expanded investor confidence. That combination drove both explosive earnings growth and aggressive valuation multiple expansion simultaneously. NVIDIA benefited from what many investors call a “double expansion cycle,” where both EPS growth and PE multiples surged together.

Today, however, the psychology is different.

The market already assumes NVIDIA will continue delivering exceptional numbers. Investors already expect Blackwell demand to remain strong. They already assume hyperscalers will continue spending aggressively on AI infrastructure. Once expectations become this elevated, even extraordinary earnings results lose some of their emotional impact on the stock price.

This explains why NVIDIA can continue producing incredible financial results without triggering the same type of violent upward moves seen in prior years.

The company still looks fundamentally dominant. The issue is that the market increasingly views that dominance as the base case rather than the upside case.

The AI Infrastructure Cycle May Still Be in Its Early Stages

Despite concerns around valuation, the broader AI infrastructure cycle still appears extremely powerful. At GTC, NVIDIA CEO Jensen Huang significantly raised long-term expectations surrounding AI data center spending, signaling confidence that the global AI buildout may continue much longer than many investors currently expect.

This is being driven by several overlapping structural forces.

Hyperscalers continue increasing AI CapEx spending as competition intensifies around large language models, AI agents, and inference infrastructure. Token consumption continues growing exponentially as AI systems become more deeply integrated into enterprise workflows and consumer applications. At the same time, sovereign AI initiatives are emerging globally as governments increasingly view AI infrastructure as a strategic national priority rather than optional technology investment.

These trends suggest the global AI infrastructure market may ultimately become much larger than current consensus estimates imply.

Sovereign AI Demand Could Become a Massive Growth Driver

One of the most underestimated themes in the AI industry today is sovereign AI infrastructure demand.

Countries across the Middle East, Europe, Southeast Asia, and parts of Asia are rapidly investing in domestic AI compute infrastructure, sovereign cloud systems, and national AI research ecosystems. Governments no longer want to depend entirely on foreign technology platforms for critical AI capabilities.

This creates an entirely new layer of AI infrastructure demand beyond traditional U.S. hyperscalers.

The Middle East in particular is emerging as a potentially major AI infrastructure hub. Several governments across the region are deploying enormous capital into AI data centers, AI supercomputing clusters, smart city infrastructure, and energy-optimized AI systems. Unlike typical enterprise spending cycles, sovereign AI projects are often tied to long-term geopolitical strategy, making them potentially more durable than standard corporate technology budgets.

For NVIDIA, this represents a powerful long-duration demand tailwind that extends well beyond Silicon Valley.

Blackwell Could Become Even Bigger Than Hopper

Another major takeaway from the quarter is the strength of the Blackwell cycle.

The market increasingly believes Blackwell may ultimately become an even larger platform transition than Hopper due to the rapid expansion of AI inference workloads and AI factory deployments. Cloud providers are no longer simply purchasing GPUs for model training. They are now building entire AI infrastructure systems designed to support persistent inference workloads, AI agents, enterprise automation, and large-scale token generation.

This distinction matters because inference demand may ultimately become far larger than training demand over time.

NVIDIA’s ability to integrate Blackwell GPUs with NVLink, InfiniBand networking, AI software stacks, and rack-scale infrastructure solutions strengthens the company’s position significantly. Rather than competing solely on chip performance, NVIDIA is increasingly competing on total system optimization.

That strategy may prove critical as the AI industry evolves.

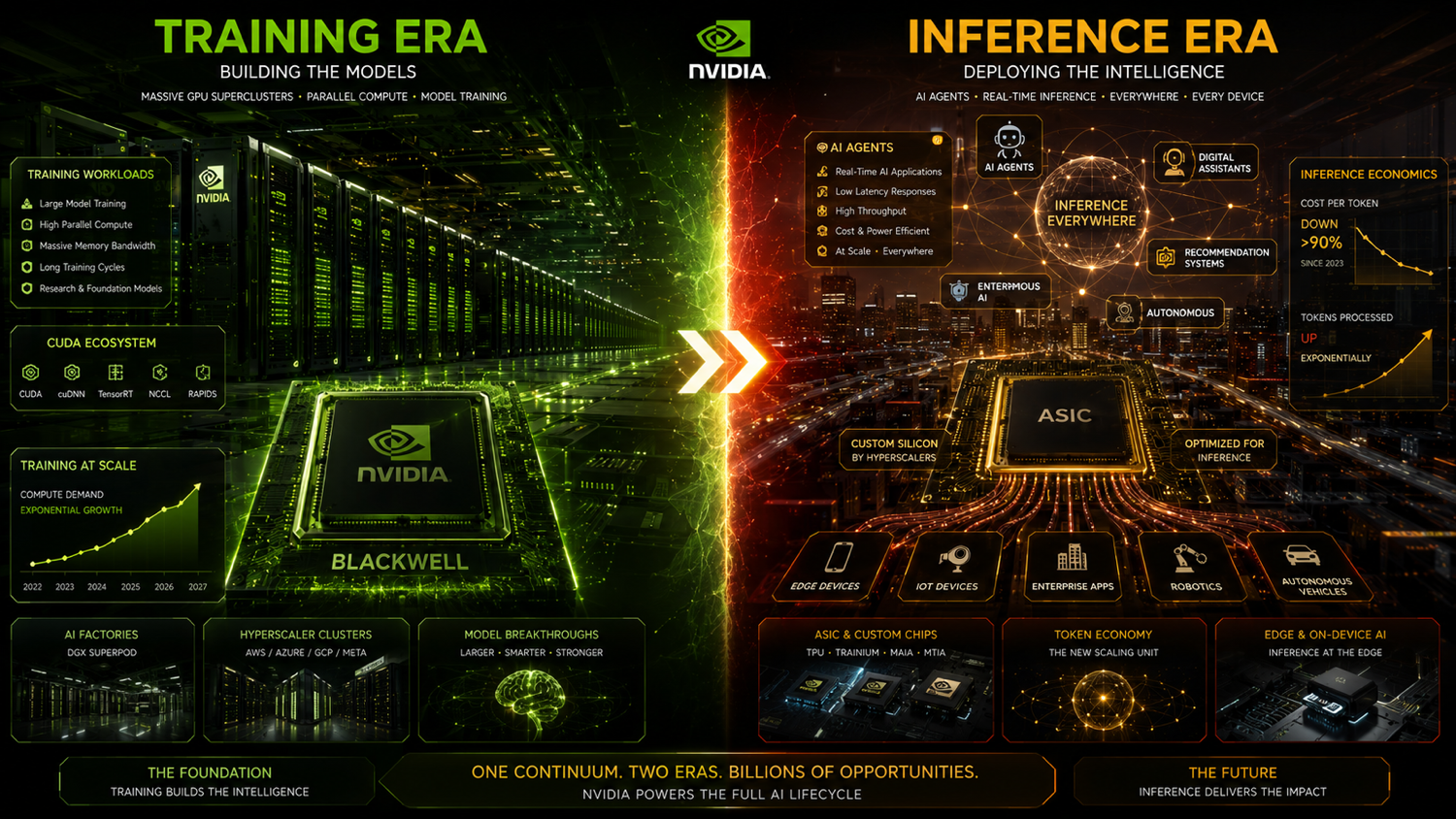

The Industry Is Transitioning From the Training Era to the Inference Era

For years, the AI race was dominated primarily by large-scale model training. During that phase, NVIDIA built an enormous lead through CUDA, GPU parallelization, networking architecture, and software ecosystem maturity.

In training workloads, NVIDIA still remains extremely difficult to challenge. The CUDA ecosystem moat remains one of the strongest advantages in the technology industry because switching costs for developers and enterprises are exceptionally high. Even companies aggressively developing internal AI chips still rely heavily on NVIDIA infrastructure.

That includes:

- Microsoft

- Amazon

- Meta

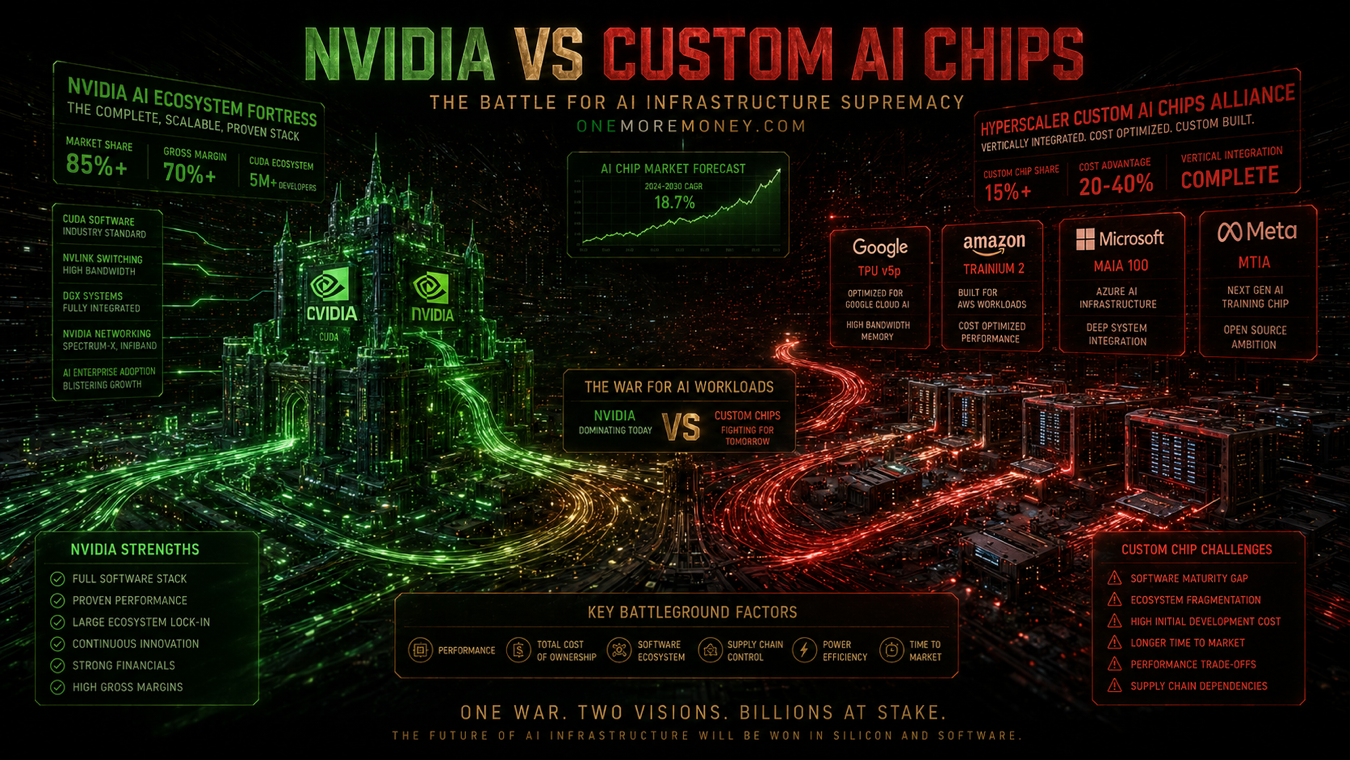

However, the economics begin changing during the inference phase.

The Architectural Shift: Moving from the massive GPU-heavy clusters of the AI training era (left) to the distributed, high-efficiency token networks and edge processors of the inference era (right).Inference workloads prioritize different metrics including cost efficiency, latency, memory optimization, deployment scale, token throughput, and power consumption. Because inference involves continuously running models rather than training them once, hyperscalers are increasingly motivated to reduce compute costs wherever possible.

This is why cloud providers are aggressively investing in custom AI chips such as:

- Google TPU

- Amazon Trainium and Inferentia

- Microsoft Maia

- Meta MTIA

The goal is not necessarily to replace NVIDIA entirely. Instead, the objective is to reduce long-term dependency on NVIDIA infrastructure and improve hyperscaler economics.

This is one of the biggest reasons investors are beginning to debate whether NVIDIA can maintain monopoly-level valuation premiums indefinitely.

The Real AI Bottlenecks Are Changing

Another major misconception in the market is the idea that GPUs remain the only bottleneck in AI infrastructure.

The industry is increasingly discovering that future AI scaling depends heavily on:

- memory bandwidth

- networking throughput

- CPU orchestration

- interconnect architecture

- power efficiency

- data movement optimization

- total system efficiency

This is precisely why NVIDIA has recently emphasized system-level AI optimization rather than purely advertising raw GPU FLOPS improvements.

The AI Hardware Standoff: NVIDIA’s dominant CUDA ecosystem fortress faces off against custom silicon architectures from tech giants—including Google’s TPU, Amazon’s Trainium, Microsoft’s Maia, and Meta’s MTIA—in a high-stakes race for AI infrastructure supremacy.The company’s strategy increasingly revolves around building fully integrated AI infrastructure systems combining:

- GPUs

- CPUs

- networking

- AI software layers

- memory architecture

- rack-scale AI systems

This is also where Vera Rubin becomes strategically important.

Vera Rubin Represents NVIDIA’s Next Strategic Expansion

NVIDIA confirmed that its next-generation Vera Rubin platform is expected to enter production during the second half of the year. While many investors focus primarily on the GPU component, the broader significance of Vera Rubin lies in NVIDIA’s attempt to deepen its role across the entire AI infrastructure stack.

The company is no longer positioning itself merely as a semiconductor supplier. It is attempting to become the foundational infrastructure layer powering AI factories, enterprise AI systems, and future AI agent ecosystems.

If successful, this transition could substantially expand NVIDIA’s total addressable market far beyond GPUs alone.

The long-term opportunity may ultimately depend less on individual chip sales and more on NVIDIA’s ability to control the broader AI infrastructure ecosystem surrounding compute, networking, orchestration, and deployment.

AI Agents Could Trigger Another Massive Compute Wave

Another increasingly important theme is the rise of AI agents.

The first phase of generative AI centered primarily around chatbot interfaces and model training. The next phase may revolve around autonomous AI systems capable of reasoning, workflow execution, multi-step decision-making, and persistent enterprise automation.

This matters because AI agents dramatically increase inference demand. Instead of isolated prompts, agentic systems continuously generate tokens, orchestrate tasks, interact with APIs, and run persistent workloads across enterprise environments.

If AI agents scale successfully across software ecosystems, inference demand could become exponentially larger than current forecasts suggest.

That possibility is one reason NVIDIA continues aggressively investing beyond traditional GPU markets into networking, AI systems, and infrastructure orchestration.

NVIDIA’s Future May Depend on Whether It Becomes an AI Platform or a Premium Hardware Supplier

The most important long-term question surrounding NVIDIA is no longer whether AI demand will continue growing.

The more important debate is whether NVIDIA ultimately evolves into:

- an AI infrastructure toll road,

or - a premium hardware supplier operating inside a more competitive ecosystem.

If NVIDIA successfully maintains dominance across CUDA, networking, AI orchestration, inference infrastructure, and system-level AI deployment, the company could sustain unusually strong platform economics for years.

However, if hyperscalers successfully reduce dependency through custom silicon, open-source ecosystems weaken CUDA’s influence, and AI infrastructure becomes increasingly standardized, valuation multiples could gradually compress even if revenue growth remains impressive.

This is why investors should increasingly monitor:

- inference market share

- CUDA ecosystem stickiness

- Vera Rubin adoption

- hyperscaler ASIC deployment

- AI networking growth

- system-level infrastructure revenue

- AI agent compute demand

These metrics may ultimately matter more than quarterly GPU shipment numbers alone.

Final Thoughts

NVIDIA’s Q1 FY2027 earnings once again confirmed that the global AI infrastructure boom remains extremely powerful. Blackwell demand continues accelerating, hyperscaler spending remains aggressive, and the company’s system-level AI strategy is expanding rapidly across networking, CPUs, and enterprise infrastructure.

At the same time, the market is entering a more psychologically complex phase.

The challenge is no longer convincing investors that NVIDIA is winning. Most investors already believe that.

The challenge now is determining how much future dominance is already reflected in the stock price.

That shift from narrative excitement toward valuation discipline may define the next era of AI investing. NVIDIA remains one of the strongest companies in the global AI ecosystem, but future returns may increasingly depend not just on growth itself, but on whether the company can sustain platform-level control across the evolving AI infrastructure economy.

Frequently Asked Questions (FAQ)

Why did NVIDIA’s stock react less aggressively despite another strong earnings report?

The market has largely shifted from questioning whether NVIDIA can continue growing to debating how much future growth is already priced into the stock. Investors now expect strong AI infrastructure demand, Blackwell adoption, and hyperscaler spending to continue. As expectations rise, earnings beats naturally create smaller emotional reactions compared to earlier stages of the AI boom.

What drove NVIDIA’s Q1 FY2027 growth?

NVIDIA’s explosive growth was primarily driven by its data center business, which benefited from accelerating AI infrastructure spending across hyperscalers and enterprises. Demand for Blackwell systems remained exceptionally strong, while AI training and inference workloads continued expanding globally.

Why is Blackwell considered so important for NVIDIA?

Blackwell is viewed as a critical next-generation AI platform because it supports increasingly complex AI training and inference workloads. Many analysts believe the Blackwell cycle could become even larger than Hopper due to the rise of AI agents, enterprise AI deployment, and persistent inference demand.

What is the difference between AI training and AI inference?

AI training involves building large AI models using massive GPU clusters and highly parallel computing systems. AI inference focuses on running trained models efficiently in real-world applications. Inference workloads prioritize cost efficiency, latency, power consumption, and deployment scale, which creates different competitive dynamics across the AI hardware market.

Why are hyperscalers developing their own AI chips?

Companies like Google, Amazon, Microsoft, and Meta are building custom AI chips to reduce long-term dependency on NVIDIA infrastructure and improve inference economics. These chips are designed to optimize power efficiency and lower operational costs for large-scale AI deployment.

What is sovereign AI demand and why does it matter?

Sovereign AI refers to governments building domestic AI infrastructure, cloud systems, and compute capacity for national strategic purposes. This trend is becoming increasingly important as countries seek technological independence and geopolitical competitiveness in artificial intelligence. Sovereign AI investment could become a major long-term growth driver for NVIDIA.

Why is CUDA considered one of NVIDIA’s biggest advantages?

CUDA is NVIDIA’s proprietary software ecosystem that enables developers to optimize AI workloads for NVIDIA hardware. Because so many AI models, enterprise systems, and developer tools are deeply integrated with CUDA, switching away from NVIDIA infrastructure can become extremely difficult and expensive.

What should investors monitor going forward?

Investors should pay close attention to:

- Blackwell adoption rates

- Vera Rubin deployment progress

- AI inference market share

- CUDA ecosystem strength

- Hyperscaler custom chip development

- AI networking growth

- AI agent infrastructure demand

- System-level AI revenue expansion

These factors may ultimately determine whether NVIDIA maintains platform-level dominance across the global AI infrastructure economy.